Intrinsic value is clearly described in the European Commission "Explanatory Notes on VAT e-commerce rules"

The Import One-Stop Shop (IOSS) scheme is applicable for the Low value goods (goods in consignments whose intrinsic value at import does not exceed EUR 150)

The "Explanatory Notes on VAT e-commerce rules Council Directive (EU) 2017/2455 Council Directive (EU) 2019/1995 Council Implementing Regulation (EU) 2019/2026" describes Intrinsic value as

(a) for commercial goods: the price of the goods themselves when sold for export to the customs territory of the Union, excluding transport and insurance costs, unless they are included in the price and not indicated separately on the invoice, and excluding any other

taxes and charges as ascertainable by the customs authorities from any relevant document(s);

(b) for goods of a non-commercial nature: the price which would have been paid for the goods

themselves if they were sold for export to the customs territory of the Union.

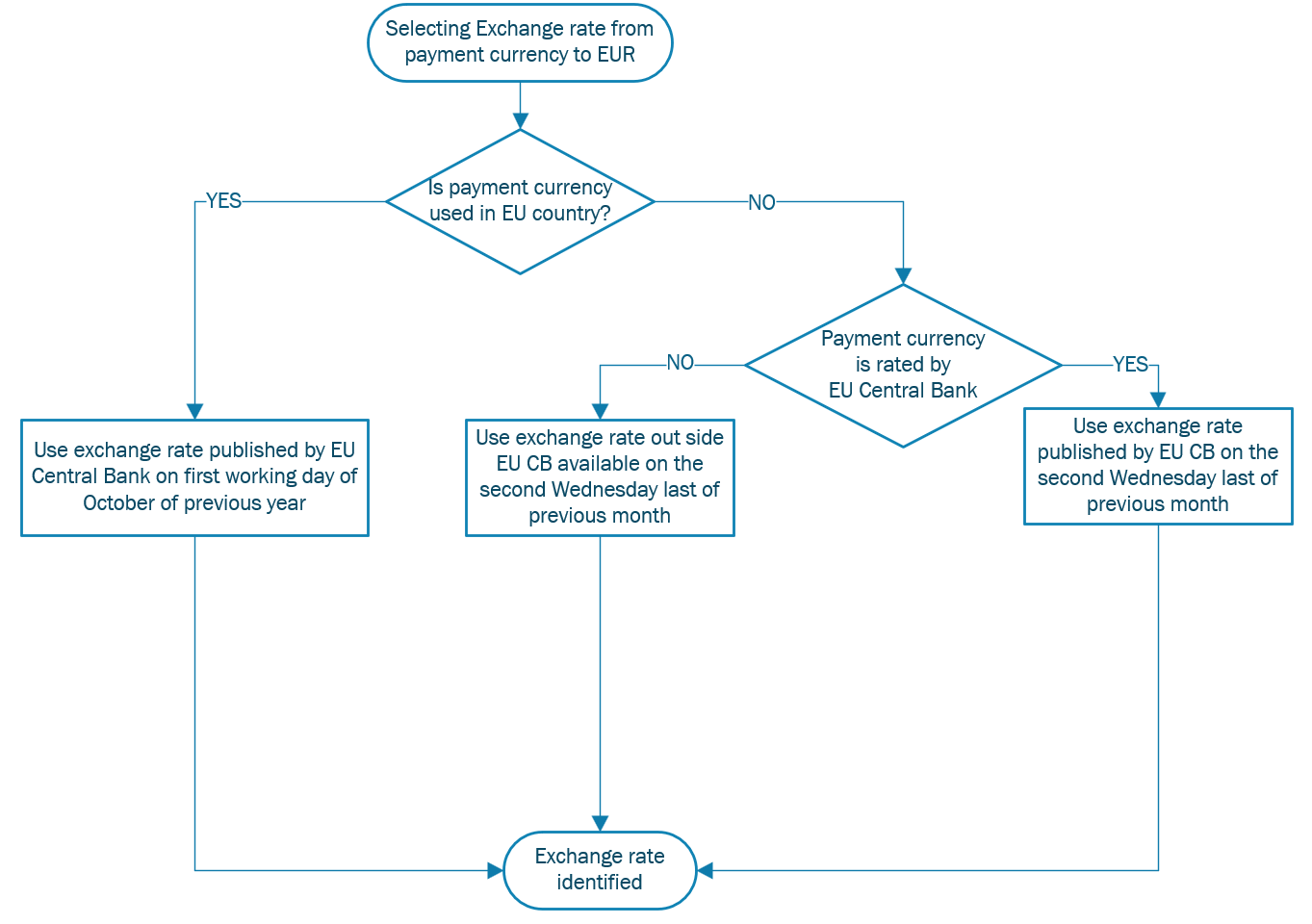

Determination of exchange rates for threshold calculation

Legal Basis

Non European Union currencies → Commission Implementing Regulation (EU) 2015/2447 Article 146 UCC Article 146

European Currencies → Commission Implementing Regulation (EU) 2015/2447 Article 369zc , Article 369l, Article 369y

Logic for exchange rate determination

GBP is considered as EU currency as it is used in the Northern Ireland (ISO country code XI)

Exchange rates used for EU currencies in 2025

| EU currency | To | Exchange rate in 2025 |

| BGN | EUR | 0.5113 |

| CZK | EUR | 0.0396 |

| DKK | EUR | 0.1341 |

| GBP | EUR | 1.2021 |

| HUF | EUR | 0.0026 |

| PLN | EUR | 0.2334 |

| RON | EUR | 0.201 |

| SEK | EUR | 0.0884 |

Several examples are presented below to clarify how to determine the intrinsic value.

Example 1: Invoice indicating total amount of the price paid for the goods not split between

net price of the goods and transport charges. VAT amount indicated separately.

| Price of the goods as indicated in the invoice: | EUR 140 |

| VAT (20%) as indicated in the invoice: | EUR 28 |

| Total invoice amount: | EUR 168 |

In this example, transport costs are not mentioned separately in the invoice and therefore

cannot be excluded. However, the net price of the goods is not exceeding EUR 150 and

therefore, IOSS can be used and no VAT or customs duties is levied at importation.

Example 2: Invoice indicating total amount of the price paid for the goods split between net

price of the goods and transport charges. VAT amount indicated separately.

| Price of the goods as indicated in the invoice: | EUR 140 |

| Transport charges as indicated in the invoice: | EUR 20 |

| VAT (20%) as indicated in the invoice: | EUR 32 |

| Total invoice amount: | EUR 192 |

In this example, transport costs are mentioned separately in the order/invoice. As such,

transport costs are excluded from the intrinsic value. The intrinsic value of the goods is not

exceeding EUR 150 and therefore, IOSS can be used and no VAT or customs duties is levied

at importation. To be noted that VAT is applied on the total value of the sale (e.g. the

EUR 160 value of the goods and the transport charges).